Restoring Utah’s Historic Homes: A Guide to Authentic Masonry

Utah’s historic homes carry a distinct architectural character shaped by regional stone, early craftsmanship, and centuries of environmental exposur

In the evolving landscape of Utah real estate, purchasing a brand-new home no longer means paying a premium. Thanks to builder-paid interest rate buydowns, buyers now have an opportunity to save tens of thousands of dollars, especially in the initial years of homeownership. This shift presents a compelling option for prospective homeowners weighing their choices between new constructions and existing homes. Understanding the financial benefits, market incentives, and practical considerations is essential for making an informed decision in Utah's competitive market.

Historically, buyers paid more for brand-new homes due to their modern features and untouched condition. However, recent market dynamics have changed this paradigm. In many Utah regions, including the greater Salt Lake City area and surrounding suburbs, home builders face increased inventory and affordability challenges. To attract buyers, builders are offering substantial incentives, including deeply discounted interest rates through programs known as interest rate buydowns.

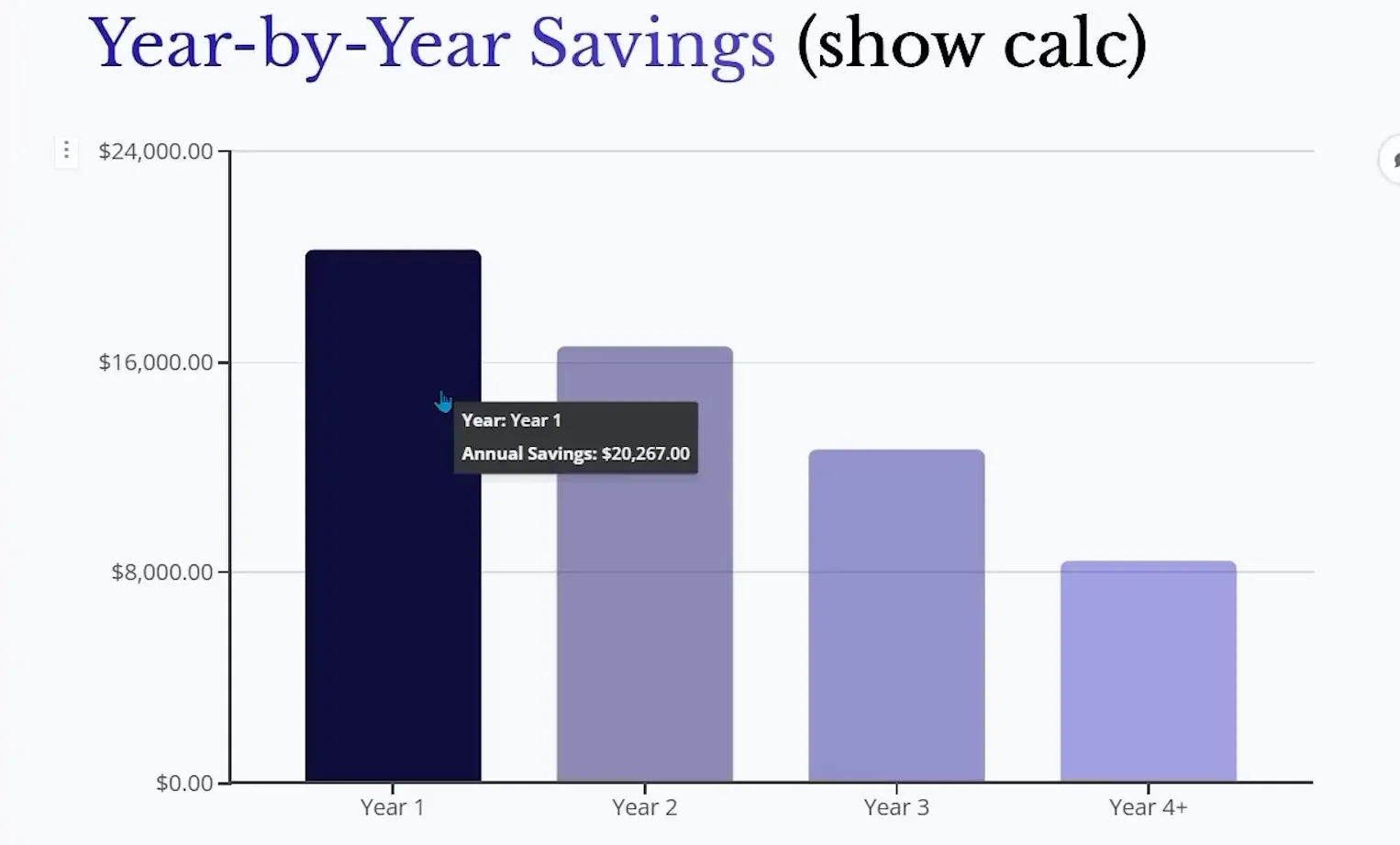

For instance, a typical new home priced at around $737,000 with a 20% down payment could qualify for a “3-2-1 buy down” interest rate structure:

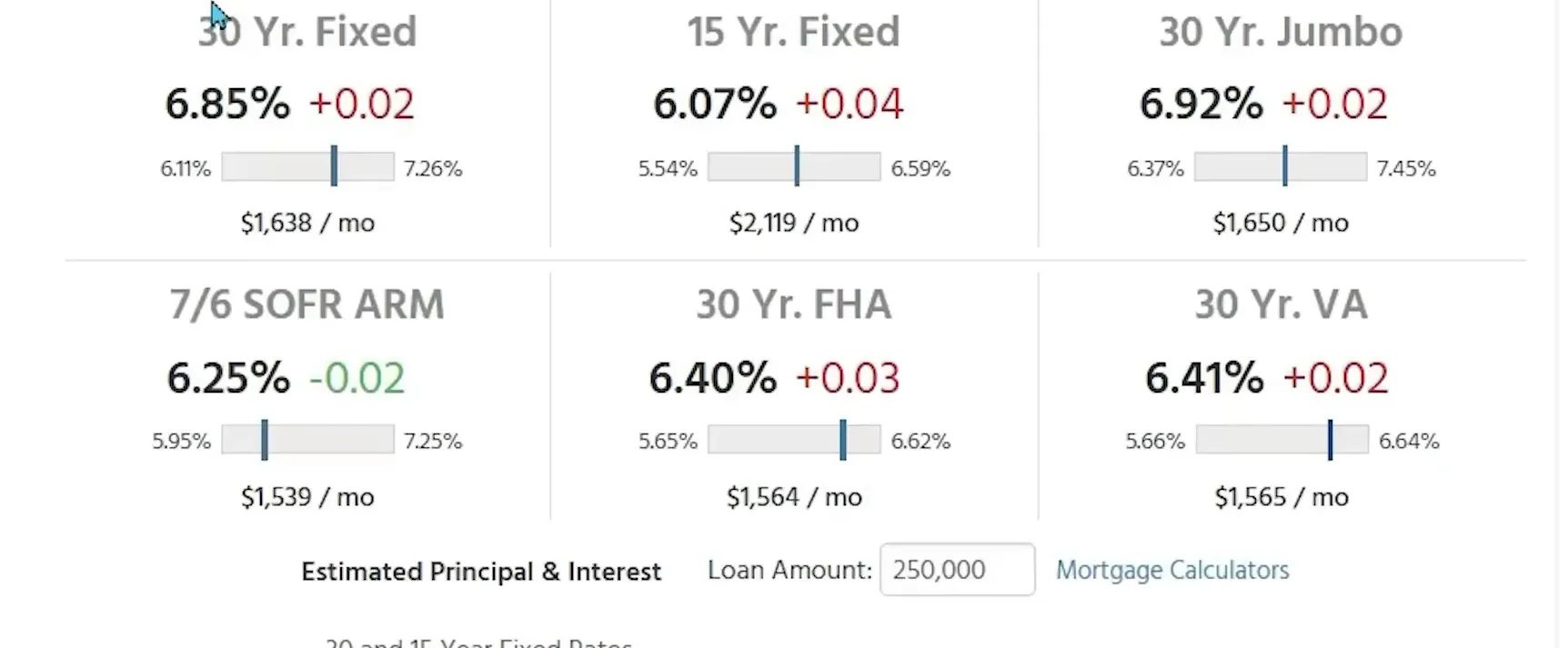

Compare this to the current average mortgage rates for existing homes, which hover around 6.85%, and the savings become clear. Monthly principal and interest payments on a new home with the buy down could start at approximately $2,200, while an older home at current rates might cost about $3,867 per month. This translates to annual savings exceeding $20,000 in the first year alone and tens of thousands over the subsequent years.

Over the first four years, buyers could save nearly $58,000 in mortgage payments alone, with continued savings of over $8,400 annually thereafter until refinancing becomes feasible at lower rates. These figures exclude property taxes, insurance, or homeowners association (HOA) fees, but even with these costs considered, new homes often remain more cost-effective.

Builder incentives are becoming more common in Utah’s new home developments, especially for move-in-ready homes. These incentives include not only interest rate buydowns but also closing cost credits and price reductions off the asking price. For example, some builders have accepted offers $40,000 below the initial listing price to move inventory quickly.

Prospective buyers should focus on completed homes rather than those still under construction or on dirt lots. Builders are more motivated to sell finished homes since the sunk costs of labor and materials have already been incurred, making these homes more likely to be offered at attractive prices and financing terms.

Sites like NewHomeSource.com provide valuable listings and incentive details, allowing buyers to evaluate options and calculate potential savings.

Utah’s real estate market offers a wide range of opportunities for buyers, from established neighborhoods in Salt Lake City and Provo to growing communities in St. George and Park City. New home construction is particularly active in suburban areas where builders compete to attract buyers with incentives and flexible financing.

Prospective buyers should leverage tools like Best Utah Real Estate to explore listings, compare neighborhoods, and connect with knowledgeable local agents. Understanding the financial mechanics behind interest rate buydowns and builder incentives can help buyers make strategic choices that align with their long-term goals.

For buyers in Utah’s dynamic real estate market, new homes offer a compelling financial advantage through builder-paid interest rate buydowns and other incentives. While location and community maturity may differ from established neighborhoods, the long-term savings, modern features, and warranties make new construction an attractive option for many. Careful evaluation of mortgage terms, builder incentives, and personal financial readiness will ensure a successful home purchase that aligns with lifestyle and investment goals.

What is an interest rate buydown, and how does it work?

An interest rate buydown is a financing incentive where the builder pays to temporarily reduce the mortgage interest rate, lowering monthly payments for the first few years. This helps buyers afford a new home despite higher baseline rates.

Are new homes always more expensive than existing homes?

Not necessarily. While new homes traditionally cost more, current builder incentives and interest rate buydowns can make new homes financially competitive or even cheaper in the short term compared to existing homes.

What should buyers watch out for in builder incentives?

Buyers should ensure the final mortgage rate after any buy down period is affordable and competitive. Temporary low rates can increase substantially, so budgeting for the eventual payment is critical.

Do new homes in Utah typically have homeowners association (HOA) fees?

Many new developments include HOAs that manage community amenities and maintenance. Fees vary widely, so buyers should review HOA bylaws and costs before purchasing.

How do property taxes affect the cost of new homes?

New homes may include additional property tax assessments to fund local infrastructure. These fees can add to annual costs but are often offset by lower maintenance and energy expenses.

Utah’s historic homes carry a distinct architectural character shaped by regional stone, early craftsmanship, and centuries of environmental exposur

Smart home improvements do more than just lower monthly utility bills. They transform a house into a modern asset that appeals to the current generation of savvy buyers. High efficiency is now a standard expectation rather than a luxury upgrade. When you focus on the right systems, you build immediate equity while creating a more comfortable living environment for your family.

St. George summers are no joke. With temperatures regularly climbing past 105°F from June through September, a working air conditioner isn't a luxury in Southern Utah it's essential.

Utah’s spring housing market is showing signs of strain. Inventory is rising, contract cancellations are elevated, rents are softening, and buyer demand is not keeping pace with the number of homes hitting the market. For anyone asking whether Utah is shifting toward a buyer’s market, the latest signals point in that direction.

Access all your saved properties, searches, notes and more.

Access all your saved properties, searches, notes and more.

Enter your email address and we will send you a link to change your password.

I agree to receive marketing and customer service calls and text messages from Best Utah Real Estate. Consent is not a condition of purchase. Msg/data rates may apply. Msg frequency varies. Reply STOP to unsubscribe. Privacy Policy & Terms of Service.

Listings displayed on this website are provided via IDX. The website owner is not the listing broker or agent unless explicitly stated.

Your trusted MLS search companion